Global Aerospace Materials Market

Market Size in USD Billion

CAGR :

%

USD

12.56 Billion

USD

21.99 Billion

2024

2032

USD

12.56 Billion

USD

21.99 Billion

2024

2032

| 2025 –2032 | |

| USD 12.56 Billion | |

| USD 21.99 Billion | |

| % | |

|

Global Aerospace Materials Market Segmentation, By Type (Aluminium Alloys, Steel Alloys, Titanium Alloys, Super Alloys, Composite Materials, Others), Aircraft Type (Commercial Aircraft, Military Aircraft, Business & General Aviation, Helicopters, Other Aircraft Types)- Industry Trends and Forecast to 2032

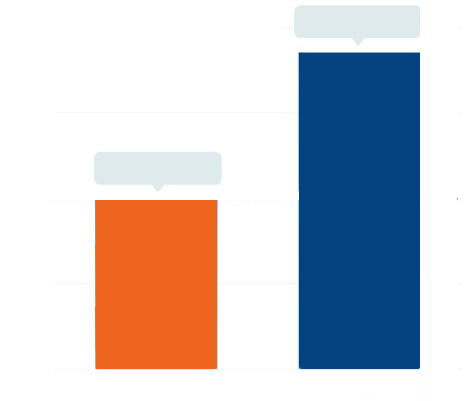

Aerospace Materials Market Size

- The global Aerospace Materials market size was valued at USD 12.56 billion in 2024 and is expected to reach USD 21.99 billion by 2032, at a CAGR of 8.7% during the forecast period

- This growth is driven by factors such as the advancement in aircraft materials, preference for composite materials and less expenditure in defence sector.

Aerospace Materials Market Analysis

- Aerospace Materials are critical components used in the manufacturing of aircraft and spacecraft, offering high strength-to-weight ratios, resistance to extreme temperatures, and durability under mechanical stress. They are essential for structures such as fuselage, wings, propulsion systems, and interior components

- The demand for these materials is significantly driven by the increasing global air traffic, rising defense budgets, and growing demand for fuel-efficient, lightweight aircraft

- North America is expected to dominate the Aerospace Materials market due to the presence of major aircraft manufacturers, strong defense spending, and established aerospace infrastructure

- Asia-Pacific is expected to be the fastest growing region in the Aerospace Materials market during the forecast period due to rapid industrialization, growing commercial aviation sector, and increasing investments in indigenous aerospace programs

- Aluminum Alloys segment is expected to dominate the market with a market share of 42.15% due to their widespread use in aircraft structures, cost-effectiveness, and favorable mechanical properties suitable for both commercial and military aircraft

Report Scope and Aerospace Materials Market Segmentation

|

Attributes |

Aerospace Materials Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Aerospace Materials Market Trends

“Integration of Advanced Composites and Lightweight Alloys in Next-Generation Aircraft”

- One prominent trend in the aerospace materials market is the increasing use of advanced composites (like carbon fiber-reinforced polymers) and lightweight metal alloys (such as titanium and aluminum-lithium) in commercial and military aircraft manufacturing

- These materials enhance aircraft performance by reducing overall weight, increasing fuel efficiency, and improving structural integrity under high-stress and high-temperature conditions.

- For instance, Boeing’s 787 Dreamliner and Airbus’s A350 XWB extensively utilize composite materials in their airframes and wings, reducing weight by up to 20% compared to traditional aluminum-intensive designs, resulting in significant fuel savings and lower emissions.

- This trend is driving innovation across the supply chain, encouraging partnerships between aerospace manufacturers and material science companies to develop durable, cost-effective, and sustainable solutions for the future of aviation

Aerospace Materials Market Dynamics

Driver

“Surging Demand for Lightweight and Fuel-Efficient Aircraft”

- The global aviation industry's push to improve fuel efficiency and reduce carbon emissions is significantly driving the demand for advanced aerospace materials

- Lightweight materials such as carbon fiber composites, aluminum-lithium alloys, and titanium alloys help reduce aircraft weight, leading to better fuel economy and lower operating costs

- As airline operators seek to modernize fleets and comply with increasingly strict environmental regulations, the adoption of innovative aerospace materials becomes critical

- For instance, In February 2023, Boeing announced that composite materials make up approximately 50% of the primary structure of its 787 Dreamliner, contributing to a 20% improvement in fuel efficiency compared to older aircraft

- As a result airlines and aircraft manufacturers strive to meet performance and sustainability goals, the demand for high-performance aerospace materials continues to grow

Opportunity

“Growth of Space Exploration and Commercial Spaceflight”

- The expanding investments in space missions by national agencies (NASA, ESA, ISRO) and private players (SpaceX, Blue Origin) are opening new avenues for aerospace materials

- Extreme environmental conditions in space demand materials with superior strength, temperature resistance, and low outgassing characteristics

- Aerospace materials are increasingly being tailored for reusability and resilience in harsh space environments, helping reduce mission costs and increase safety

- For instance, In March 2024, SpaceX’s Starship utilized stainless steel and other high-performance alloys designed to withstand both launch stress and re-entry heat, underscoring the importance of material innovation in next-gen space vehicles

- The expanding sector creates opportunities for material suppliers to develop and commercialize specialized materials for rockets, space stations, and satellites.

Restraint/Challenge

“High Costs and Complex Manufacturing Processes”

- The production of advanced aerospace materials, such as carbon fiber composites and titanium alloys, involves complex processes and high capital investments

- These high production costs often translate into expensive end products, limiting widespread adoption—particularly among smaller aerospace firms and in price-sensitive markets

- In addition, materials like carbon fiber require long production cycles and specialized labor, further contributing to delivery delays and cost overruns

- For instance, In December 2024, according to an industry report by Deloitte, the cost of carbon fiber composites remains approximately 5–10 times higher than aluminum, posing a barrier to broader implementation in commercial aviation, especially in budget-sensitive sectors

- Consequently, such economic and operational hurdles slow down market penetration and adoption, particularly in emerging markets, thus challenging the overall growth trajectory

Aerospace Materials Market Scope

The market is segmented on the basis Type and Aircraft Type

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Aircraft Type |

|

In 2025, the aluminium alloys is projected to dominate the market with a largest share in Type segment

The aluminium alloys segment is expected to dominate the Aerospace Materials market with the largest share of 42.15% due to their widespread use in aircraft structures, cost-effectiveness, and favorable mechanical properties suitable for both commercial and military aircraft.

The commercial aircraft is expected to account for the largest share during the forecast period in aircraft type market

In 2025, the commercial aircraft segment is expected to dominate the market with the largest market share of 51.31% due to increasing global air traffic, fleet modernization programs, and a growing emphasis on fuel-efficient aircraft. As the backbone of the aviation industry, commercial aircraft demand a high volume of advanced materials such as aluminum alloys, carbon fiber composites, and titanium to enhance fuel efficiency, safety, and performance.

Aerospace Materials Market Regional Analysis

“North America Holds the Largest Share in the Aerospace Materials Market”

- North America dominates the Aerospace Materials market, driven by the presence of leading aircraft manufacturers, high defense spending, and strong investments in research and innovation for next-generation materials

- The U.S. holds a significant share due to increasing demand for lightweight and fuel-efficient commercial aircraft, modernization of military fleets, and growing adoption of composite and advanced alloy materials

- Federal initiatives supporting sustainable aviation and partnerships between aerospace OEMs and material developers further reinforce the region’s leadership

- In addition, a mature aerospace supply chain, skilled workforce, and well-established regulatory framework support continuous market expansion across the region

“Asia-Pacific is Projected to Register the Highest CAGR in the Aerospace Materials Market”

- The Asia-Pacific region is expected to witness the highest growth rate in the Aerospace Materials market, fueled by rapid industrialization, expanding commercial aviation sector, and increased defense procurement programs

- Countries such as China, India, and Japan are emerging as key markets due to rising air passenger traffic, growth of low-cost carriers, and strong government support for domestic aerospace manufacturing

- Japan, with its advanced engineering capabilities and strong focus on aerospace R&D, plays a crucial role in driving innovation in materials and manufacturing processes

- China and India, with their massive aerospace ambitions and expanding fleets, are witnessing increased investments in aerospace infrastructure and partnerships with global material suppliers, further boosting market growth in the region

Aerospace Materials Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, Type dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Alcoa Corporation (U.S.)

- Aleris Corporation (U.S.)

- AMG Advanced Metallurgical Group (Netherlands)

- AMI Metals (U.S.)

- Air Transport International, Inc. (U.S.)

- Avdel (U.K.)

- Constellium (Netherlands)

- Solvay (Belgium)

- DOW (U.S.)

- Hexcel Corporation (U.S.)

- Hindalco - Almex Aerospace Limited (India)

- Kaiser Aluminum (U.S.)

- KOBE STEEL, LTD (Japan)

- Koninklijke Ten Cate bv. (Netherlands)

- Lee Aerospace (U.S.)

- Materion Corporation (U.S.)

- PARK AEROSPACE CORP (U.S.)

- Renegade Materials Corporation (U.S.)

- SGL Carbon (Germany)

- TATA Advanced Materials Limited (India)

- Sofitec Aero, S.L. (Spain)

Latest Developments in Global Aerospace Materials Market

- In March 2025, Hexcel Corporation announced the expansion of its manufacturing facility in Morocco to meet growing demand for advanced composites used in commercial aerospace. The expansion will enhance the production of honeycomb core materials, crucial for lightweight aircraft structures, and support Hexcel’s global supply chain for Airbus and Boeing programs.

- In February 2025, Solvay introduced a new high-performance thermoplastic composite material designed for next-generation single-aisle aircraft. The material offers superior fatigue resistance and is compatible with automated manufacturing, enabling faster production cycles and lighter airframe designs while reducing environmental impact.

- In January 2025, Kaiser Aluminum Corporation signed a multi-year supply agreement with a major commercial aircraft OEM to provide advanced aluminum-lithium alloy products for fuselage and wing components. This strategic deal underscores the increasing adoption of aluminum-lithium alloys to enhance aircraft efficiency and reduce weight.

- In December 2024, SGL Carbon partnered with a European space agency to develop heat-resistant carbon composite materials for reusable space vehicles. These materials are engineered to withstand extreme temperatures and are aimed at enhancing re-entry performance and lifespan of space components.

- In November 2024, TATA Advanced Materials Limited announced the successful delivery of composite structural components for a new defense aircraft program in India. This marks a significant milestone in the company’s efforts to support indigenous aerospace manufacturing and reduce dependency on imported materials.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Aerospace Materials Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Aerospace Materials Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Aerospace Materials Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.